Week of January 17, 2021

Silver, Slavery, and Soil Quality

This week, we explore a range of empirical studies in economic development, including the two quite modern examples of Xu and Derenoncourt. Their papers are excellent examples of how to make a concrete argument in economic history, centering on novel databases assembled through record digitization and properly using causal inference in a range of conservative specifications. We’ll also look at some classic works, too, including Robert Allen’s critique of the Marxian “enclosure-efficiency” hypothesis and the famed North and Weingast analysis of the Glorious Revolution.

Was Slavery Central to America’s Development?

Bradley A. Hansen | Bradley A. Hansen’s Blog | June 11, 2018

In short, no. Hansen disputes the widely-held view—especially among conventional historians—that slave-driven industries in the antebellum South, especially cotton, were essential components of America’s economic rise by showing the comparatively minor role that they played in the economy. By calculating the shares of cotton in agricultural output, of agriculture in commodities, and of commodities in total product, Hansen finds that the cotton industry accounted for at most 5.8 percent of GDP in 1860. Cotton textiles, meanwhile, composed 3.9 percent. He convincingly refutes the secondary claim that enormous spillovers resulted from cotton production, adding that one could adduce additional benefits from any sector, including wheat. Hansen concludes that slavery and slave-based industries were important, but hardly crucial, factors in American development. This is essential reading, given the extent to which the claims of scholars like Edward Baptist—who receives some pithy insults here—have become accepted wisdom in academic circles.

American Precious Metals and Their Consequences for Early Modern Europe

Nuno Palma | Handbook of the History of Money and Currency | December 19, 2019

Popular histories of the colonization of the Americas emphasize the central role that the extraction of silver played in the subsequent Great Divergence between Europe and Asia. Palma, however, convincingly shows that Spain and Portugal—the “first-order receivers” of the yields from Potosi and Brazil—actually suffered economically in the long run, especially compared to “second-order” receivers like Britain and the Netherlands. The Iberian countries derived short-run boosts to demand and liquidity, such that wage and price stickiness increased GDP, but ultimately saw soaring inflation erode the performance of their export sectors and the quality of their institutions. The nations of northern Europe, meanwhile, saw inflows primarily through increased product demand, and so experienced genuine economic booms. Moreover, “[t]he increased availability of precious metals “allowed for a substantial increase in the monetization and liquidity levels of the economy decreasing transaction costs, increasing market thickness, changing the relative incentive for participating in the market, and allowing agglomeration economies to arise.” The problem of “small change” was resolved by increased holdings of currency (decreased in value), allowing for a range of inexpensive purchases to occur.

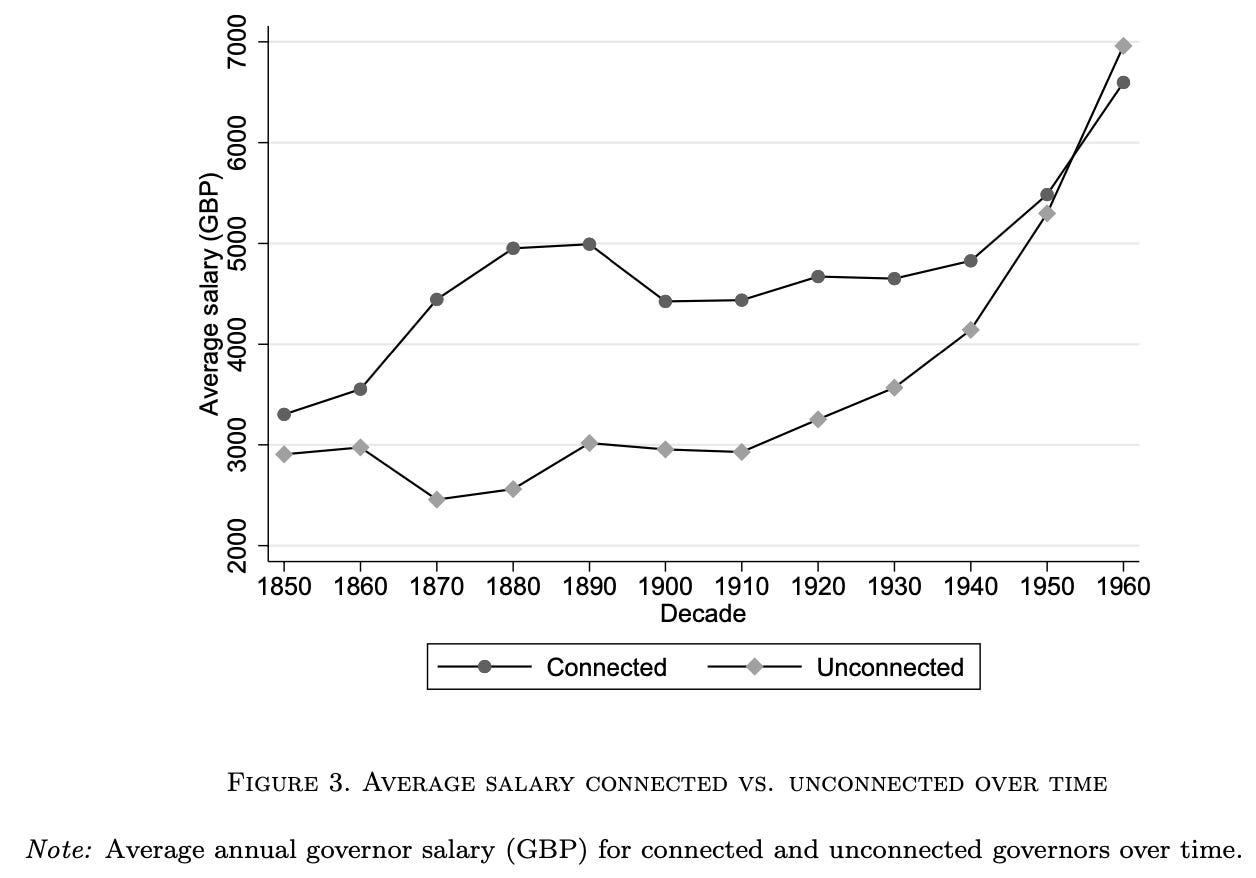

The Costs of Patronage: Evidence from the British Empire

Guo Xu | American Economic Review | 2018

Having painstaking assembled a biographical database of the British aristocracy, Xu sets out to prove that colonies whose governors were related—by blood or social ties—to the incumbent Secretary of State for the Colonies suffered from poor economic performance as a result of adverse incentives. He alternately regresses salaries and revenues on a binary measure of relatedness, based on “shared ancestry, membership of groups like the aristocracy or the attendance of the same elite school or university,” and demonstrates that the presence of these bonds had a powerful affect on executive quality. Governors with connections to “patrons” personally earned salaries 10 percent above their less advantaged counterparts while generating 4 percent less revenue. The former was achieved by unearned promotions to larger or more prosperous colonies, while the latter resulted from patronage governors’ dispersal of undue tax exemptions to placate local elites. The effect disappears after the Warren Hastings reform of 1930, which established oversight committees for appointments. A subsequent paper published the following year demonstrates an even more remarkable consequence: that the reductions in economic performance during patronage periods, in turn, lowered the fiscal capacity of the colonies after independence.

Atlantic slavery’s impact on European and British economic development

Ellora Derenoncourt | Working Paper | 2018

Using new datasets on slaving voyages and aggregate trade levels, Derenoncourt revisits the Williams thesis, which holds that the Atlantic slave trade provided the financing required for the Industrial Revolution in Britain. Using a relatively straightforward fixed effects regression, she shows that a 10 percent increase in slaving voyages originating from a city is associated with a 1.2 percent rise in population. By assembling data on overall trade volume from port books stored in the British National Archives, she demonstrates that this trend is separable from the concurrent process of Atlantic urbanization resulting from regular commerce. Derenoncourt suggests three channels through which slaving may have developed Western Europe: direct profits, credit expansion, and trans-oceanic market integration. There seems to be some room for doubt given that no control for pan-European urbanization is used, but this remains a streamlined and parsimonious paper.

The Efficiency and Distributional Consequences of Eighteenth Century Enclosures

Robert C. Allen | The Economic Journal | December 1982

Rejecting received wisdom, Allen argues that the enclosure movement—which raised rents across England during the seventeenth and eighteenth centuries—did not actually raise farm productivity. He compares two explanations for higher rents, elevated yields and redistribution, and shows that the former is unlikely, given that initial comparisons suggest that open-field farms were more productive than closed counterparts. After controlling for environmental factors, such as soil quality, rainfall, and heat, differences in efficiency are no longer statistically significant. Allen suggests that the cause of rising rents was actually the renegotiation of leases at the time of enclosure, which resulted in the redistribution of a larger share of the surplus to landlords. Open-field rents, he speculates, may have been lower than the value of the land would have entailed because of collective bargaining by the farmers, who could negotiate reductions in exchange for modernizing practices (which they otherwise had no incentive to do). This last claim appears doubtful, suggesting a sociological argument concerning a “peasant mode of production” that has proved empirically flawed (as in last week’s Clark paper). Nevertheless, the article is a brilliant critique of a common-sensical but ultimately naive claim.

Douglass North and Barry Weingast | The Journal of Economic History | December 1989

Probably the canonical example of institutional analysis in history, “North and Weingast 1989” proposes that the Glorious Revolution, when Parliament bloodlessly overthrew James II and installed William III of Orange as monarch, improved English governance and consequently economic performance. The establishment of “parliamentary supremacy” led to an “institutional redesign” which ended the string of “arbitrary” exactions levied by the monarchy in the years preceding the English Civil War, giving the kingdom “credible commitment” to honoring financial claims. The property rights of private citizens became more secure, encouraging investment and economic activity, while the sovereign was able to borrow enormous sums, increasingly liquidity and market depth.

Explicit limits on the Crown's ability unilaterally to alter the terms of its agreements played a key role here, for after the Glorious Revolution the Crown had to obtain Parliamentary assent to changes in its agreements. As Parliament represented wealth holders, its increased role markedly reduced the king's ability to renege. Moreover, the institutional structure that evolved after 1688 did not provide incentives for Parliament to replace the Crown and itself engage in similar "irresponsible" behavior. As a consequence the new institutions produced a marked increase in the security of private rights.

The chief body of evidence for this dramatic shift in institutional quality is not an arbitrary governance index, as AJR and others have since used, but the contrast between rising Crown debt after 1689 and stagnant or even declining interest rates. This part is suspect, having been criticized by Clark (and more recently by Paul Schmelzing) on the grounds that neither property rights nor capital markets became more favorable, having already been so in the lead-up to the Civil War. Nevertheless, the fact that debt ballooned without occasioning a spike in interest rates does suggest that the new regime was perceived in a fundamentally different light by investors. The authors conclude that the consequences of this change included an increasingly powerful state, capital accumulation (as private rates fell), securities trading, and the spread of banks. All of these factors would be crucial during the coming century in producing the Industrial Revolution.