The Bulletin

Week of July 11, 2021

Since many new readers subscribed during the last week, I thought that I’d start with a brief explanation of the usual publication format and lay out my aims for the future. Each week, I summarize my notes on three to four recent economic history papers that I’ve found insightful and provocative. I plan to—but don’t hold me to this!—write longer-form essays every second or third week, though, so if you’re mainly looking for that sort of content, it’s coming. I’m now also contemplating turning this into an “Open Thread” a la Astral Codex Ten, so if you have interesting things to say, feel free to comment, and we can see where this goes. If not, I’m going to keep releasing these anyway.

This week’s readings include a new bibliographical index of patent quality, a history of American bank failures, a comparison of branch lending in Tokugawa Japan and industrial England, and an analysis of the municipal capital market in 19th century Britain. Enjoy!

Patterns of innovation during the Industrial Revolution: A reappraisal using a composite indicator of patent quality

Alessandro Nuvolari, Valentina Tartari, and Matteo Tranchero | Explorations in Economic History

Now thirty years old, Joel Mokyr’s two-phase description of technological innovation is still pervasive in economic history. Paradigmatic macroinventions spring to life “ab nihilo,” transforming fields and industries; microinventions incrementally improve on these strokes of “genius” by tinkering and refinement.1 Quantifying the rate of innovation in these categories is difficult. One literature has sought to use patenting volume, but accounting for the relative importance of each submission has been challenging. Nuvolari et al devise a new indicator, the “Bibliographic Composite Index,” based on Bennet Woodcroft’s Reference Index of Patents of Invention, 1617–1852. The measure aggregates the “visibility” of the invention in the Woodcroft book and modern reference works, as well as that of the inventor in biographical dictionaries.2 Testing this dataset justifies Mokyr’s distinction between macro- and microinventions; further, macroinventions occur “serendipitously” (as Mokyr suggests), while microinventions “cluster,” being correlated with the business cycle.3 Additionally, the cited macroinventions do—support Robert Allen’s High Wage Explanation—display a labor-saving bias, but the creators were usually “engineering specialists” rather than “outsiders” to the trades. Following Crafts (2011), the authors argue that their findings suggest a compromise in the Mokyr-Allen controversy.

EDIT: Anton Howes reminds me that Mokyr’s definition (see above) is based not on importance, but novelty: a “radical new idea” may have no effect at all, while small, incremental improvements to existing designs—such as Kay’s flying shuttle—can vastly increase worker productivity. Macroinventions, furthermore, are not “General Purpose Technologies,” and microinvention is not synonymous with “learning-by-doing.” Mokyr’s intent was, for better or worse, to distinguish between inventions that might arise from economic incentives and those that seemed to be truly original.4

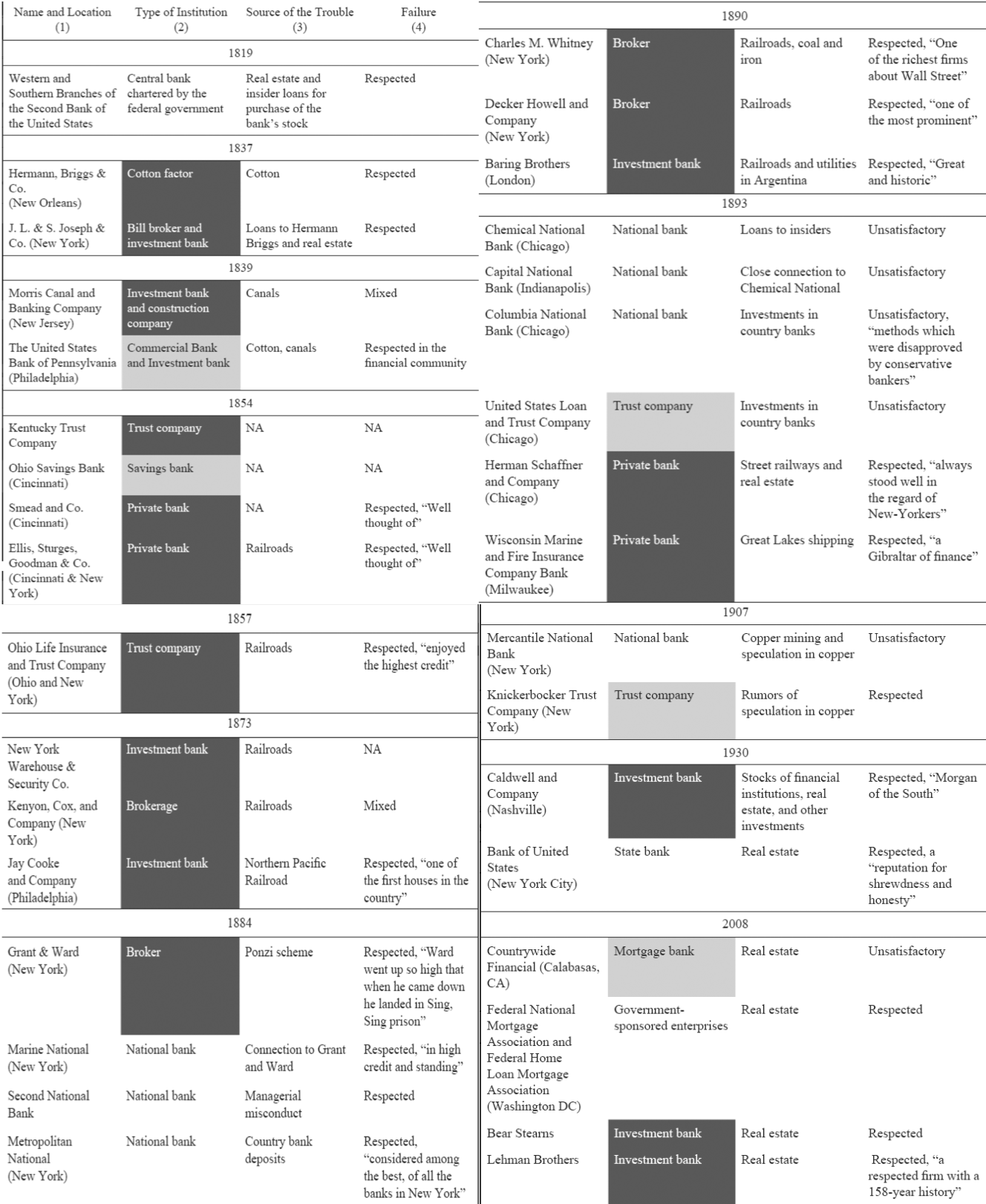

Oh, How the Mighty Have Fallen: The Bank Failures and Near Failures That Started America’s Greatest Financial Panics

Hugh Rockoff | The Journal of Economic History

The financial history of the United States is littered with banking panics, of which the crash of 2008 was just one nostalgic reminder. Rockoff considers 12 such events taking place over the last two centuries, starting with the Panic of 1819, winding through 1873, 1907, and 1930, and arriving on our doorstep with the mortgage crisis. He finds that this succession of micro-dramas is bound together by four main themes. First, banking crises usually start with a small series of failures that erode confidence. Second, many of the institutions that failed were “shadow banks,” as in 2008, as well as in 9 of the other 11 cases. The nineteenth century, in particular, saw a host of private banks, brokers, and investment banks caught out by Panglossian plays on railways. Third, practically all failing institutions had over-invested in real estate assets, engaging in the same kind of gross speculation that nailed Lehman Brothers and Bear Stearns just over a decade ago. Finally (and most insidiously), the collapsing banks had unimpeachable reputations to the very last. “It is when banks that we thought were sound go under,” Rockoff writes, “that we change our estimation of the soundness of the financial system.” In other words, we don’t know how bad things are until we can’t do anything about it.

Metropolitan Financial Agents and the Emergence of Inter-regional Financial Linkages in England and Japan, 1760-1860

Mina Ishizu | LSE Working Paper

Here’s a good question in comparative history: why wasn’t Japan England (or vice versa)? Both were commercialized island nations endowed with strong state capacity, natural and human capital, and temperate climates, and both would prove economically precocious—at a century’s remove. Ishizu’s work suggests that, at least in the financial sector, the similarities were superficial. Both countries had two tiers of metropolitan agents at the center of a provincial branch network. London’s West End goldsmiths lent bullion to the public and crown, holding the assets of the wealthy, but were in decline after 1730, being replaced by the famous “City bankers” and their discount houses. In Tokugawa-era Osaka, meanwhile, money changers—charged with converting in-kind rice taxes to silver—analogous roles; debasements in the early eighteenth century led to their proliferation, from 155 in 1700 to 532 in 1759. These institutions provided sufficient liquidity and carried enough capital that 90 percent of all transactions in the city were conducted on commercial paper. But while in 1812 90 percent of provincial towns with branch banks had correspondent relationships with the City, only 19 percent did in Japan—where profits for metropolitan agents acting outside Osaka were mediocre (as opposed to the British discount business). The Meiji confirmed the lack of endogenous financial development by trying to import both a correspondent system and the practice of bill discounting from the West. The absence of a country bank system would have been likely to hinder provincial business investment at a time when industrial towns were rising at significant distances from metropolitan sources of capital. If the inadequacies of Britain’s country banking system led most corporate finance to be conducted through plowed-back profits (and donations from relations), how damaging might this have been for scaling Japanese rural enterprise?

Making the municipal capital market in nineteenth-century England

Ian Webster | Economic History Review

Thanks to Charles Dickens and Friedrich Engels, we look upon the early industrial town with horror. Supine under belching chimneys and noxious smoke, ridden with crumbling alleys and flooded with toxic water, England’s cities have been marked out as catastrophic failures in the provision of public goods. Jeffrey Williamson, in his excellent Coping with City Growth during the British Industrial Revolution (1990), has slated the British government for under-investing in social overhead capital—sanitation, public health, and housing—in a period when urbanization leaped from 26 to 65 percent in a single century. Improved sanitation, for example, would have repaid five times in productivity gains any marginal increase in spending. In any event, the central government lacked the resources, and the municipalities were constrained by property holders aghast at an increase in the rents. Webster’s paper examines how municipal governments used the capital market to evade these constraints. He assembles a new database describing the size, performance, and participants in municipal lending, and finds—in contrast to the present—that private creditors predominated. Difficulties in removing sewage and supplying clean water forced councils to borrow extensively, initially by using non-tradable mortgages on the local rates, which supplied more than sufficient capital until 1860. Rising expenditures on waste disposal in London, however, led the Metropolitan Board of Works to issue tradable stock, which—after a brief period of skepticism—eventually became oversubscribed and provided a third of municipal financing. The author favorably compares Britain’s decentralized model with the American bond market of the present.

The full passage, from The Lever of Riches (1990): “I define microinventions as the small, incremental steps that improve, adapt, and streamline existing techniques already in use, reducing costs, improving form and function, increasing durability, and reducing energy and raw material requirements. Macroinventions, on the other hand, are those inventions in which a radical new idea, without clear precedent, emerges more or less ab nihilo. In terms of sheer numbers, Microinventions are far more frequent and account for most gains in productivity. Macroinventions, however, are equally crucial in technological history.”

“For each patent we count the number of times it is mentioned in this set of sources, obtaining in this way a quality score that we call Patent Eminence (PAT_EM).”

This entails an economic motivation for microinventions—as systematic adjustments and improvements of existing technologies—but not macroinventions, which Allen had argued were responses to relative factor prices.